Most people only think about their credit file when something has gone wrong — a finance application got declined, a hardship notice landed in the mail, or someone mentioned a credit score in conversation and they couldn't remember the last time they'd checked theirs. By that point the file has usually been doing its quiet work for years, building a picture of who you are as a borrower that every lender in Australia uses to decide whether to approve you, what to charge you, and how much they're willing to lend.

This guide walks through what a credit file actually contains, the 11 factors that influence it most, and what we as brokers see when we look at a client's file before placing an asset finance application. It's also the explainer we wished existed when our clients first ask "but how do they decide?"

What a credit file is

A credit file is the record that credit reporting bodies — primarily Equifax, Experian, and illion in Australia — hold about your borrowing history. Every time you apply for finance, take out a credit product, miss a repayment, or have a default recorded against you, that information generally ends up on your file. When a lender assesses your application, they pull a copy of that file and use it to inform their decision.

You have one consumer credit file (personal) and, if you've operated under an ABN, a commercial credit file (business). Lenders typically check both when assessing finance for ABN holders.

The 11 factors that influence your credit file

Below are the categories most credit reporting models weigh. They are not equally weighted — some matter more than others, and the relative importance differs slightly between credit bureaus — but each one shows up somewhere in how lenders read your file.

1. Account repayment history

This is the single most influential factor on most credit files. Repayment History Information (RHI) shows whether each of your active accounts — credit cards, personal loans, mortgages, telco bills above $150 — was paid on time for each of the last 24 months. A single missed payment doesn't sink a file, but a pattern of late payments will.

What this means at application time: lenders are looking at this column-by-column. Three "late by 30 days" markers in the last 12 months will tell a lender far more about your reliability than a clean file with one one-off default from 2019.

2. Consumer adverse information

This category covers court writs, default judgments, bankruptcies, debt agreements, and other adverse legal events. The presence of these — or their absence — can dramatically change what's possible. A paid-out default from years ago is a different story to an active hardship arrangement currently in place.

Australian credit reporting rules limit how long this information stays on a file. Defaults typically remain visible for five years. Bankruptcies remain visible for the term of the bankruptcy plus two years (minimum five). Older entries fall off — which is one reason credit files can improve materially over time without you doing anything specific.

3. Type of credit provider

Lenders look at the who of your prior credit, not just the what. A history of borrowing from major banks reads differently to a history of payday lenders, debt consolidators, or buy-now-pay-later operators. There may be different levels of risk associated with a bank-issued personal loan compared to a high-cost short-term lender — and credit models reflect that.

This isn't about judging your past choices. It's about lenders calibrating risk based on the company you've kept on your file.

4. The type and size of credit

Different credit products carry different risk profiles. Mortgages, credit cards, personal loans, store finance, and asset finance all sit in different categories. A file showing a long-standing mortgage with no missed payments tells a different story to a file showing six personal loans taken out across the last 18 months.

Lenders look at the mix as well as the amount — how much credit you have access to, how much you're using, and how diverse the types are.

5. Number of credit applications

Every time you apply for credit, an enquiry gets logged on your file. A single enquiry has minimal impact. Multiple enquiries in a short period — particularly for the same product type — can flag what's called "credit hungry behaviour" and concern lenders.

This is one of the biggest reasons asset finance brokers exist. A broker submits one application to the right lender, rather than letting you shotgun applications across multiple lenders and rack up enquiries that hurt your file. More on this in the broker section below.

6. Directorship and proprietorship information

If you've been a director, officer, or proprietor of a business — current or past — that information sits on your commercial credit file. Lenders look at the financial track record of those businesses, any insolvency events, and the responsibilities you held within them.

For ABN holders applying for asset finance — particularly under low-doc arrangements — this matters significantly. A director's history with previous companies is part of the lender's assessment of you as an applicant.

7. Age of credit report

A brand-new credit file with very little history tells lenders less than an established one with years of clean repayment behaviour. A new file isn't a problem — every credit file starts somewhere — but a newer file may indicate a different level of risk than an older report.

Building a positive credit history takes time. There's no shortcut, but there are accelerants: keeping a small credit card or low-balance personal loan active and paying it down on time is one of the most reliable ways to build the depth that lenders look for.

8. Historical pattern of credit enquiries

Beyond the raw number of enquiries, lenders look at the pattern. A file showing many credit applications clustered over a short period reads as higher risk than an older file with only a few enquiries. Spacing matters. Type matters. Whether the enquiries resulted in approvals matters.

This is also where being declined repeatedly can hurt you twice over — once because the underlying issue triggered the decline, and again because the pattern of enquiries makes the next lender more cautious.

9. Commercial address information

The location and length of residence at a current business address can signal stability. A business that has operated from the same address for five years reads differently to one that has moved three times in twelve months. Stability — in address, in director details, in trading history — is something lenders value highly because instability often correlates with operational stress.

10. Identity details

Identity-level information — name, date of birth, addresses, employment — all sits on the credit file. Length of employment with a single employer can provide insight into stability. A pattern of frequent address changes can sometimes trigger fraud checks or stability questions.

Keep your identity details up to date with your bank, the ATO, and the electoral roll. Credit bureaus pull from these and other sources, and mismatched details can occasionally cause delays at application time.

11. Recency vs depth of file

A short file with recent activity is different to a long file with very little recent activity. Lenders want to see that your file is both deep (history) and recent (active). A file that has been dormant for a long time, even if the prior history was perfect, often needs to be rebuilt before sharper rates become available.

Ready to get started?

Book a chat with an Asset Finance Broker at Treadgold Finance today.

What lenders actually do with your credit file

Lenders don't just look at one number. They run your file through their internal scorecards — proprietary models that weigh the 11 factors above (and a handful of others) against the loan you're applying for. The decision they're making is essentially:

"Given everything we know about this applicant's borrowing history, what is the likelihood they'll repay this specific loan on time?"

The answer feeds into three things: whether to approve, what rate to charge, and what loan structure to offer.

What changes between lenders is which factors carry the most weight. Some lenders are very strict on enquiry count but flexible on prior defaults. Some are tough on adverse information but soft on file age. Others penalise non-bank lender history heavily.

This is why two applicants with what looks like the same credit file can get very different responses from the same lender — and why the right lender for one file is the wrong lender for another.

How a finance application affects your file

Every formal finance application generates a credit enquiry on your file. The enquiry is recorded with the date, the lender, the type of credit applied for, and the outcome (approved, declined, withdrawn). Enquiries stay on your file for around five years.

A single enquiry on its own has minimal impact. Two or three across a couple of years is normal. Six in a year — especially if some were declined — is a problem.

This is the practical reason brokers exist. A broker doesn't just compare lenders for you; the broker also protects your file by submitting to a single, well-targeted lender rather than chasing approvals across many.

What to do before applying for finance

A few weeks before you plan to apply for asset finance — vehicle, equipment, caravan, business — there are practical steps worth taking:

Check your file. You're entitled to a free copy of your credit file from each of the three credit bureaus once per year (or once every three months if you've been declined or had identity issues). Look for errors, old defaults that should have dropped off, and anything that doesn't match what you'd expect.

Pay down credit card balances. Lenders look at credit utilisation — how much of your available credit you're using. A card with a $10,000 limit that's at $9,500 is a different signal to the same card at $1,500.

Consider consolidating multiple debts. If you're carrying balances across several credit cards or short-term loans, refinancing them into a single facility can reduce your utilisation ratio across your file and simplify what lenders see when they assess you.

Don't take on new credit. In the 30 days before you apply for asset finance, avoid signing up for new credit cards, BNPL accounts, or other credit products. Each application is an enquiry.

Settle small disputes. If you have a telco bill in dispute, a small unpaid account, or anything in collection, deal with it before applying. Even small adverse markers can shift a lender's decision.

Get your documents organised. Bank statements, payslips, BAS, and ID documents ready before you start the application means the broker can place your file faster and the lender's decision arrives quicker.

How brokers protect your credit file

Here's the part most borrowers don't realise about how brokers actually help — beyond comparing rates.

One application, not many. A broker assesses your file and circumstances, identifies the lender most likely to approve and offer competitive terms, and submits one application. You don't end up with five lender enquiries on your file from a self-directed scattergun approach.

Pre-assessment without the enquiry. Most asset finance brokers can review your situation and indicate likely approval before a formal enquiry is logged. This is sometimes called a soft pre-assessment. It means you find out where you stand without burning a credit enquiry on every conversation.

Matched lender appetite. Lenders don't publish their internal rules. A broker who's placed hundreds of asset finance deals knows which lender currently has appetite for self-employed applicants, which one is tougher on credit enquiries, which one is most flexible on older defaults. That matching is what produces an approval first time rather than three declines in a row.

Honest disclosure upfront. Telling your broker about a default from three years ago or a current ATO payment plan saves time and prevents wasted enquiries. We can usually still help — but only if we know what's on the file before we apply.

Treadgold Finance is an asset finance brokerage based on the Sunshine Coast with an Australian Credit Licence and access to more than 40 lenders. We arrange finance across vehicles, equipment, caravans, trucks, business cash flow, and personal asset purchases.

If you'd like a pre-application chat about your credit file before you commit to anything formal, we're happy to have that conversation. No enquiry is logged at that stage — we just look at your situation and give you a realistic picture of where you stand and what lenders are most likely to fit.

Frequently Asked Questions

How do I check my credit file in Australia?

You can request a free copy of your file from each of the three credit reporting bodies — Equifax, Experian, and illion — once every 12 months, or every 3 months if you've been declined for credit recently or had identity-related issues. Each bureau has a free request form on its website. Avoid third-party services that charge for what you can get directly for free.

Does checking my own credit file affect my score?

No. Checking your own file is what's called a "soft enquiry" and doesn't affect your credit score or what lenders see. Only "hard enquiries" (formal credit applications) appear on your file in a way that affects lender assessment.

How long do defaults stay on my credit file?

Most defaults remain visible for five years from the date they were listed. Court judgments and bankruptcies have different timeframes — bankruptcies remain visible for the term of the bankruptcy plus two years (minimum five years total).

Can I improve my credit file before applying for finance?

Yes, though most improvements take time to show. The fastest wins are: paying down credit card balances, ensuring all current accounts are paid on time, settling any small disputed amounts, and avoiding new credit applications in the lead-up. Building positive Repayment History Information takes consistent on-time payments over months.Yes, though most improvements take time to show. The fastest wins are: paying down credit card balances, ensuring all current accounts are paid on time, settling any small disputed amounts, and avoiding new credit applications in the lead-up. Building positive Repayment History Information takes consistent on-time payments over months.

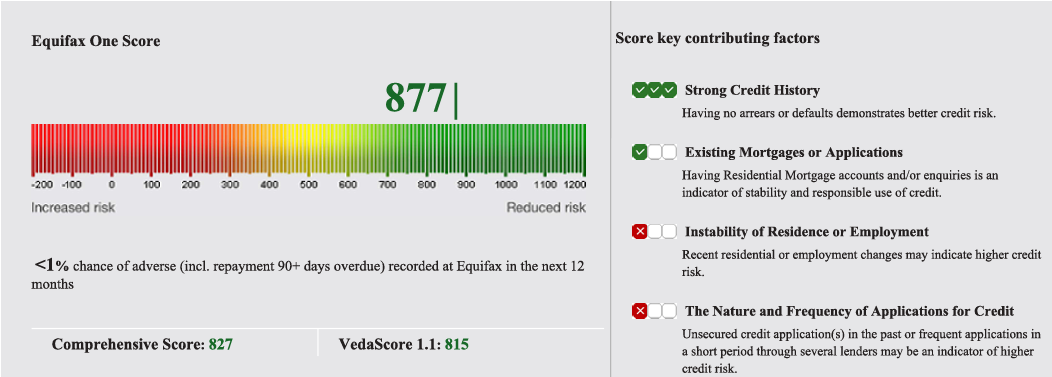

What's the difference between my credit file and my credit score?

Your credit file is the full record of your borrowing history — every account, enquiry, default, and address change. Your credit score is a number (typically 0–1,200 in Australia) calculated from that file using a scoring model. Different bureaus use different models, so your score can differ slightly between Equifax, Experian, and illion. Lenders typically look at both the score and the underlying file.

Will a broker look at my credit file before applying?

Most asset finance brokers will do a pre-assessment based on what you tell them about your file before logging any formal enquiry. If you have a recent copy of your file, sharing it with your broker upfront helps them target the right lender first time rather than guessing.

Can I get finance with a default on my file?

In many cases yes, depending on the nature, age, and amount of the default. A paid-out telco default from three years ago is a very different story to an active default on a major credit account. There are specialist lenders that fund borrowers with prior credit issues, though the rates are generally higher. A broker can identify which lenders currently have appetite for your specific situation.